Best Ages to Start an Indexed Universal Life (IUL) Policy Age-Based IUL Highlights 0–18: Start early for maximum growth. Great for college or future wealth. 20–35: Low premiums + time. Ideal for retirement and long-term goals. 36–50: Still affordable. Great for tax-free retirement planning. 51–65: Best for legacy & estate planning. Needs higher funding. 66+: Primarily for wealth transfer. Limited cash value growth. Suitability Table Age Range 0–18 20–35 36–50 51–65 66+ Suitability Best Use College funding, future growth Retirement, long-term savings Tax-free income planning Estate & legacy goals Wealth transfer only (it looked like this: )

Best Ages to Start an Indexed Universal Life (IUL)

Policy Ages 0–18 (Children & ‘Million Dollar Baby’ Plans) Ultra-low premiums + decades of compound growth Used for college, wealth-building, and future borrowing Parents/grandparents fund early for big long-term benefits Ages 20–35 (Young Adults) Affordable premiums + long time horizon Great for retirement savings or early financial planning Lock in low rates while healthy; build strong cash value Ages 36–50 (Peak Earning Years) Strong income allows for aggressive funding Still time to grow significant cash value Used for tax-free retirement or wealth planning Ages 51–65 (Later Starters) Works best with larger premiums or lump sums Best for estate planning and legacy goals Cash value growth may be slower Ages 66+ Not ideal for growth, but valuable for wealth transfer Often used with long-term care or death benefit focus Premiums are high and require careful planning Quick Reference Table Age Range 0–18 20–35 36–50 51–65 66+ Suitability for IUL Best Use College funding, wealth transfer Tax-free retirement, loan access Supplement retirement, protect income Estate planning, legacy Legacy only, not cash growth

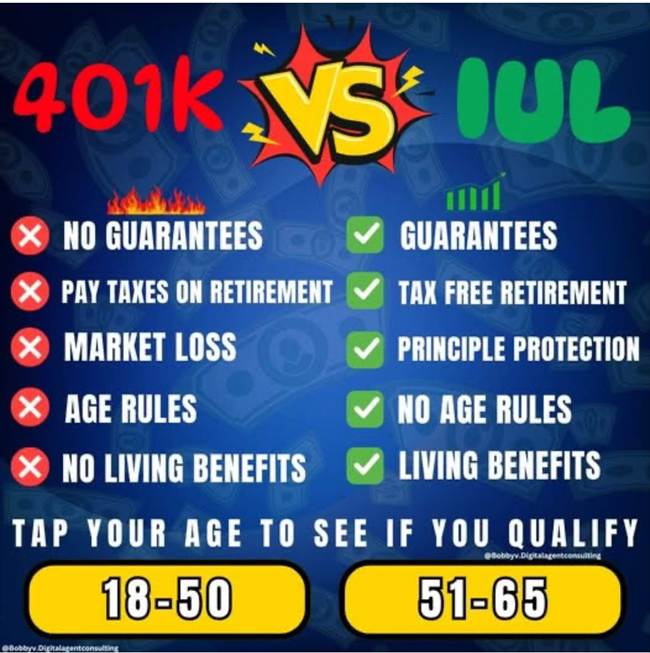

Looks like:

Whole Life vs. Indexed Universal Life (IUL)

Here’s a quick and clear comparison to help your clients choose the life insurance plan that fits their financial goals and risk comfort. Premiums Whole Life: Fixed for life IUL: Flexible, can adjust over time Cash Value Whole Life: Guaranteed growth IUL: Market-indexed (not guaranteed) Risk Level Whole Life: Very low risk IUL: Moderate risk with caps/floors Death Benefit Whole Life: Guaranteed IUL: Performance-dependent Best For Whole Life: Stability & estate planning IUL: Growth potential & flexibility Need help deciding? Let’s find the best policy to protect your future and grow your legacy.